ABSTRACT

“A strong economy is the source of national strength.”

Insolvency and bankruptcy code,2016 is the second most crucial reform in the legal setting of India. It is because Insolvency and bankruptcy code is not only making India emphatically powerful in the field of the legal environment but also provides a new identification and recognition at the global platform economically. The Insolvency and Bankruptcy Code, 2016 is the bankruptcy law of India which seeks to consolidate the existing framework by creating a single law for insolvency and bankruptcy. The paper studies distinguish features and the legal framework of the code. The study is descriptive in nature. In line with that, the paper also presents the impact of Insolvency and Bankruptcy code on macro environment of India.

KEYWORDS

Insolvency and bankruptcy code,2016, Macro Environment, Insolvency, Bankruptcy, Legal Environment of India, Liquidation.

INTRODUCTION

Insolvency is a situation where individuals or companies are unable to repay their outstanding debt. The legal status of an entity or a person where the debt owed to the creditors cannot be repaid is known as Bankruptcy.

It is a legal declaration of one’s inability to pay off debts. A court order imposes bankruptcy in most of the jurisdictions. It is mostly initiated by the debtor. It is important to note that bankruptcy is not synonymous with insolvency. It is not the only legal status that could be applicable to an insolvent individual or an entity. In countries like the UK, bankruptcy is exclusive to individuals. Liquidation, administration and other such insolvency proceedings are applicable to entities and companies.

The Insolvency and Bankruptcy Code, 2016 (IBC) is the bankruptcy law of India which seeks to consolidate the existing framework by creating a single law for insolvency and bankruptcy.

The IBC was considered a major effort in resolving the issues of NPAs which had been plaguing the Indian banking Industry and the rising corporate borrowing defaults.

The IBC lays down separate processes of insolvency resolution for Companies, individual borrowers and partnership firms. For effective functioning the code provides for 2 Adjudicating authorities namely NCLT and DRT. While resolving Insolvency cases of companies rested in the hands of NCLT, DRT handled the resolution process of Insolvency cases of individuals and partnership firms. IBC laid down strict time bound resolution process and in effect had a target of resolving insolvencies in a time span of 270 days.

RESEARCH METHODOLOGY

The descriptive, observational and secondary quantitative data-based analysis is conducted to understand the legal provisions of insolvency and bankruptcy in India and the impacts of Covid-19. The data collected is mostly from sources of various books, journals, articles, annual reports published by the government and websites of different governmental and non-governmental agencies and organizations.

REVIEW OF LITERATURE

- Renuka Sane (2019):- The researcher has the view that government had only notified corporate insolvency and not the personal insolvency when it passed the IBC in 2016. The author says that the scenario of Indian credit market calls for the need for the personal insolvency law. The paper was a brief presentation of the provisions on personal insolvency in the IBC. The author makes suggestions on questions of policy which are required to be addressed prior to the meaningful implementation of Law so as to ensure proper design of the subordinate legislation as well as the evolution of the institutional infrastructure. The author is of the opinion that debt to GDP ratio in India is much smaller as compared to other emerging or developed economies. As per the author NPAs on personal loans from the banking sector are comparatively smaller in contrast to the industrial loans still their continually rising nature calls for addressal of personal insolvency issues even.

The author raises serious concerns over agricultural lending and the fact that the stress from informal lending remains un known . Only institutional credit has recourse to legal processes which leaves other types of lenders without any legal channel of recovery. The researcher in her paper provides a brief overview of the legal provisions in the law. As per the researcher the prime motivation in drafting of the law was its potential impact on the credit market in India. A brief discussion on the distinctive processes for dealing with default has been carried out which includes the “Fresh Start” process providing debt-waiver to debtors who meet certain eligibility conditions as far as income, assets and debts are concerned. The researcher has the opinion that the success of the IBC depends on the design of the subordinate legislation as well as the evolution of the institutional infrastructure.

- Pratik Datta(2018):- In this study the researcher has applied theoretical concepts to analyze the major problems like value destruction and wealth transfer in new code of Insolvency and Bankruptcy. The author has identified four potential sources of wealth transfer under the Insolvency and Bankruptcy Code, 2016. The Indian policymakers has to revisit the fundamental legislative design choices embedded within the Insolvency and Bankruptcy Code, 2016 to successfully address the contemporary concerns regarding the value destruction and wealth transfer problems.

- Nakul Sharma,2 Dr. Rahul Vyas(2017):- The paper studies the Insolvency Professional Agency framework in terms of its role, which is the bulwark of the IBC in terms of the procedural and regulatory ambit of the code. The IBC 2016 is a landmark development in the law of our country which provides resolution in a time bound manner, promotes entrepreneurship which will lead to an improvement in credit availability and would balance interest of all stakeholders.

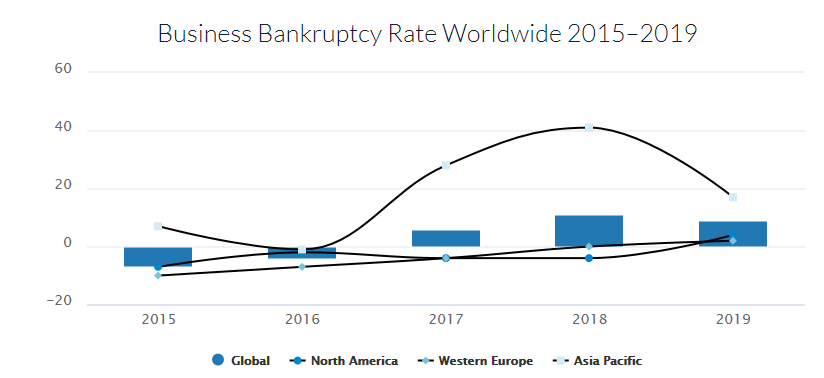

GLOBAL BANKRUPTCIES STATISTICS

- At the global level, the 9% year-over-year upward trend in business insolvencies continued in 2019

- North America is on a reversal trend at 3% increase, along with Western Europe at a 2% rise.

- From 2016 to 2020, business failures are expected to consistently rise by 6% year-over-year.

- Asia will be the key contributor to the 8% year-over-year rise in business bankruptcies in 2020.

BACKGROUND

In India, the legal and institutional machinery for dealing with debt defaults has not yet been in line with global standards. The recovery action of the creditors, either through the Contract Act or through the special laws such as the Recovery of Debts due to Banks and Financial Institutions Act, 1993 and the Securitization and Reconstruction of Financial Assets an Enforcement of Security Interest Act, 2002, has not been able to get the desired outcomes. Similarly, action through the Sick Industrial Companies (Special Provisions) Act, 1985 and the winding up provisions of the Companies Act, 1956/Companies Act, 2013 have neither been able to aid the recovery for lenders nor aided in the restructuring of firms. Laws dealing with individual insolvency, Presidential Towns Insolvency Act, 1909 and the Provincial Insolvency Act, 1920 are almost a century old. This has hampered the confidence of the lenders over the period of time. The ‘Insolvency and Bankruptcy Code, 2016’is considered the biggest economic reform next to GST. The Insolvency and Bankruptcy Code 2016 is landmark legislation consolidating the regulatory framework governing the restructuring and liquidation of persons (including incorporated and unincorporated entities).

The objective of the new law is to promote entrepreneurship, availability of credit, and to balance the interests of all stakeholders by consolidating and amending the laws relating to reorganization and insolvency resolution of corporate persons, partnership firms and individuals in a time-bound manner and for maximization of value of assets of such persons and matters connected therewith or incidental thereto. It aims to consolidate the laws relating to insolvency of companies and limited liability entities (including limited liability partnerships and other entities with limited liability), unlimited liability partnerships and individuals, presently contained ina number of legislation, into a single legislation. Such consolidation will provide for greater clarity in the law and facilitate the application of consistent and coherent provisions to different stakeholders affected by the business failure or inability to pay the debt.

VARIOUS BIILS

The Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018

The Ordinance amends the Insolvency and Bankruptcy Code, 2016 to clarify that allottees under a real estate project should be treated as financial creditors.

The voting threshold for routine decisions taken by the committee of creditors has been reduced from 75% to 51%. For certain key decisions, this threshold has been reduced to 66%.

The Ordinance allows the withdrawal of a resolution application submitted to the NCLT under the Code. This decision can be taken with the approval of 90% of the committee of creditors.

Insolvency and Bankruptcy Code (Amendment) Bill 2019

The Code provides a time-bound process for resolving insolvency in companies and among individuals. Insolvency is a situation where individuals or companies are unable to repay their outstanding debt.

Under the Code, a financial creditor may file an application before the National Company Law Tribunal (NCLT) for initiating the insolvency resolution process. The NCLT must find the existence of default within 14 days. Thereafter, a Committee of Creditors (CoC) consisting of financial creditors will be constituted for taking decisions regarding insolvency resolution. The CoC may either decide to restructure the debtor’s debt by preparing a resolution plan or liquidate the debtor’s assets.

The CoC will appoint a resolution professional who will present a resolution plan to the CoC. The CoC must approve a resolution plan, and the resolution process must be completed within 180 days. This may be extended by a period of up to 90 days if the extension is approved by NCLT.

If the resolution plan is rejected by the CoC, the debtor will go into liquidation. The Code provides an order of priority for the distribution of assets in case of liquidation of the debtor. This order places financial creditors ahead of operational creditors (e.g., suppliers). In a 2018 Amendment, homebuyers who paid advances to a developer were to be considered as financial creditors. They would be represented by an insolvency professional appointed by NCLT.

The Bill addresses three issues. First, it strengthens provisions related to time-limits. Second, it specifies the minimum payouts to operational creditors in any resolution plan. Third, it specifies the manner in which the representative of a group of financial creditors (such as home-buyers) should vote.

Insolvency & Bankruptcy Code (Second Amendment) Act 2020

Rajya Sabha recently passed an Insolvency & Bankruptcy Code (2nd amendment) Act 2020.

The IBC Bill 2020 came into force on June 5th, 2020.

After section 10 of the Insolvency and Bankruptcy Code, 2016 the following section shall be inserted –

Section 10 A – Suspension of initiation of the corporate insolvency resolution process. As per Section 10 A, ‘Notwithstanding anything contained in sections 7, 9 and 10, no application for initiation of corporate insolvency resolution process of a corporate debtor shall be filed, for

any default arising on or after 25th March, 2020 for a period of six months or such further period, not exceeding one year from such date’. Fresh insolvency proceedings will not be initiated for at least six months starting from March 25 amid the COVID-19 pandemic.

Default on repayments from March 25, the day when the nationwide lockdown began to curb COVID-19 infections, would not be considered for initiating insolvency proceedings for at least six months.

Amendment of section 66. In section 66 of the principal Act, after sub-section (2), the following sub-section shall be inserted –

” Section 3 – “Notwithstanding anything contained in this section, no application shall be filed by a resolution professional under sub-section (2), in respect of such default against which initiation of the corporate insolvency resolution process is suspended as per section 10A.”

The ordinance suspends sections 7, 9, and 10 on grounds that the pandemic has created uncertainty and stress for business for reasons beyond their control, the nationwide lockdown has added to disruption of normal business operations in such circumstances it would be difficult to find an adequate number of resolution applicants for a distressed/defaulting business.

The Insolvency and Bankruptcy Code (Amendment) Bill, 2021

The Insolvency and Bankruptcy Code (Amendment) Bill, 2021 was introduced in the Lok Sabha to amend the insolvency law and provide for a prepackaged resolution process for stressed Micro, Small and Medium Enterprises.

The bill will replace the ordinance that was promulgated on April 4 this year. It proposed ‘pre-packs as an insolvency resolution mechanism for MSMEs.

under this mechanism, main stakeholders such as creditors and shareholders come together to identify a prospective buyer and negotiate instead of a public bidding process.

Provisions of the Bill:

- It specifies a minimum threshold of not more than Rs 1 crore for initiating the pre-packaged insolvency resolution process

- It provides for disposal of simultaneous applications for initiation of the insolvency resolution process and pre-packaged insolvency resolution process, pending against the same corporate debtor.

- Penalty for fraudulent or malicious initiation of pre-packaged insolvency resolution process or with intent to defraud persons, and for fraudulent management of the corporate debtor during the process.

- Punishment for offences related to the pre-packaged insolvency resolution process.

NEED FOR BANKRUPTCY LAW

According to central bank data, stressed assets rose to 14.5% of banking sector loans at the end of December 2015. There is almost Rs 10 trillion of loans that are stuck. India’s banking industry was the state of crisis. Bad debts are piling up at the banks. Multiplicity of laws has been a problem in the way of banks failing to recover their loans.

IMPACT OF THE BANKRUPTCY ACT

With the addition of the Bankruptcy and Insolvency Code, the Indian lending system has gotten teeth in dealing with stressed borrowers and a difficult macroeconomic situation.

- Impact of the bankruptcy code will be widely positive, leading to a better management of stressed companies in India .

- Insolvency resolution is important for investments, whether Indian or foreign capital,

- As the Indian banking system stares at a Rs6.3 trillion bad loan pile, a legal stress resolution mechanism is the need of the hour.

- There will be better financial discipline among companies, which will work to ensure that all their creditors are paid on time.

- the powers have once again come into the hands of lenders as they are far above equity holders in the payout structure that the code mandates in a liquidation situation.

ECONOMIC SURVEY, 2019-20

The Economic Survey of the Government of India for 2019-20 noted the progress made under the IBC since its enactment, in terms of its use by stakeholders and the development of an ecosystem of service providers. The realizations under the IBC for Financial Creditors and time taken for the same were noted as being better than those under other available avenues for resolving distressed assets in the country.

EASE OF DOING BUSINESS REPORT, 2020

The Ease of Doing Business Report assesses 190 economies in terms of 10 parameters that span the lifecycle of a business as to how conducive the environment is for doing business in an economy. According to the Report 2020, India’s overall ranking improved by 14 places to 63rd position among 190 countries as against last year’s 77th position. With this India earned a place among the world’s top ten improvers in ease of doing business, for the third consecutive year.

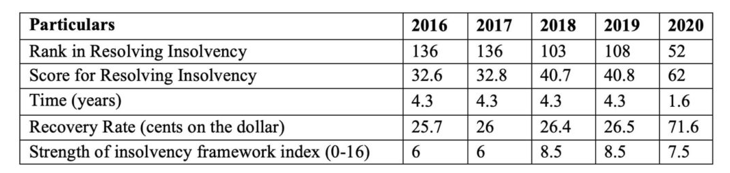

In the ‘resolving insolvency’ parameter, India’s ranking improved 56 places to 52 this year from 108 last year. As per this report, owing to the establishment of a modern insolvency regime with the enactment of the IBC, India made resolving insolvency easier by promoting reorganisation proceedings in practice. As a result, the overall recovery rate for creditors jumped from 26.5 to 71.6 cents on the dollar and the time taken for resolving insolvency also came down significantly from 4.3 years to 1.6 years.

Here’s a view of India’s journey in the ‘resolving insolvency’ parameters, according to Ease of Doing Business Reports over the past few years.

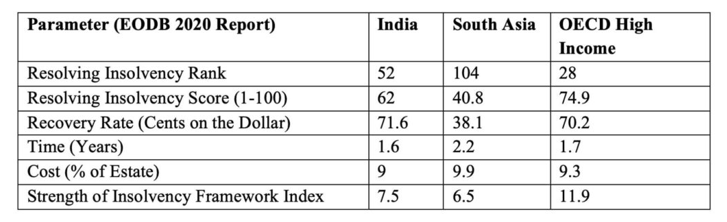

India is now, by far, the best performer in South Asia on the resolving insolvency component and does better than the average for OECD high-income economies in terms of recovery rate, time taken and cost of a corporate insolvency resolution process, the Ease of Doing Business 2020 Report noted.

IMPACT OF COVID-19

Covid-19 had a threatening influence all over the world. The era of the pandemic had forced the government authority to bring combating measures so that they can cure the increasing rates of havoc. Moreover, they hold a strong intention to blow out all the increasing Covid – 19 cases worldwide. Therefore, focusing on the above-mentioned objectives, a nationwide lockdown was declared by our Honorable Prime Minister.

The Indian government passed the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2020, which suspends the application of Sections 7, 9, and 10. The emergence of Covid-19 has caused a massive economic meltdown, which has led to the collapse of numerous industries including MSMEs, tourism, health care, and automobiles. As a result, in order to resolve court issues in terms of the IBC, the focus switched to the reconstruction and protection of various business stakeholders.

The exclusion of lockdown period and the increased threshold limit are welcome steps taken by the legislature to ensure that the Micro, Small and Medium Enterprises have enough cushion to recover from the financial distress caused by the COVID-19 pandemic and would also declutter the cases under IBC by filtering out the frivolous ones.

It is ought to be remembered that the operational creditors do not stand to benefit in case a company undergoes liquidation as they are below the financial creditors in the line of proportionate repayment. The IBC is only a measure of last resort for the operational creditors. However, in cases where there is a personal guarantee, mostly given by the promoters/directors, it might still be used as a mechanism for recovery as the limit for initiation of the proceedings has not proportionately been increased and could possibly be a route that may be used to put pressure on the companies.

Nevertheless, in the times of the unprecedented downturn being experienced on account of the COVID-19 pandemic, the aforesaid measures would prove to be beneficial for resurrection of the enterprises facing the heat. After all, the key objective of the IBC is to ensure that the corporate debtor keeps operating as a going concern.

CONCLUSION

There has been a marked improvement in the recovery process which is already leading to billions of dollars being invested in the country due to the protection of creditor rights. Compared to other markets, the pace at which we have achieved this is also noteworthy.

The IBC, like any other piece of law, has had a revolutionary effect. Unlike previous regimes, the IBC has been positively received by the system and is being used in a way that is enhancing stakeholder value.

Because the government has been proactive in ensuring that issues are addressed, the courts have avoided overturning the COC’s decisions, with the exception of a few stray judgments. After the Coronavirus pandemic has been effectively managed, the government will focus its efforts on ensuring that the code is implemented decisively and fully operational.

“The economy is the start and end of everything. We cannot have successful education reform or any other reform if we do not have a strong economy.”

NAME: ANKITA SINGH

YEAR: SECOND (2nd)

COLLEGE: S.S. KHANNA GIRLS’ DEGRE COLLEGE [UNIVERSITY OF ALLAHABAD]