“Corporate social responsibility” (CSR) talks about how firms operate to use social, environmental, and economic initiatives to improve society as a whole. It is also known as social performance, sustainable responsible business, corporate conscience, or corporate citizenship. The long-term economic success of society is essential to the survival of business. CSR is not a novel idea. Our country is the first nation in the world to impose statutory compliance requirements on CSR spending. CSR is essential to a business’s expansion and helps it establish a positive public image. It’s undeniably a business strategy that builds long-term value for customers and employees by taking into account all aspects of how a business functions in the social, cultural, and environmental domains in addition to developing a “green strategy” for the environment.

The paper is aimed at understanding the concept of CSR and the legal framework governing it and also deals with the impacts of CSR on the corporate performance of the business and the recent trends in the Indian scenario.

KEYWORDS

Corporate Social Responsibility, Company, CSR Activities, Corporate Performance, Charity, Sustainable development.

INTRODUCTION

‘Profit maximization is the sole motive of a business’ is what has been considered the mindset of a businessman while entering the corporate world. A business that operates in the real world has to interact with various stakeholders. It is society from which a business flourishes, and it is the ethical obligation of a business to contribute to it. This idea of “giving back to society” is what we call Corporate Social Responsibility. Corporate social responsibility is the Corporate Conscience of the business, which ensures its survival by fostering long-term prosperity in the future.

Corporate social responsibility is a management concept that deals with how companies accommodate social and environmental issues in their operations and interactions with their stakeholders. “It is a “Triple-Bottom-Line- Approach” to achieving balance between economic, social, and environmental fundamentals while dealing with the expectations of shareholders and stakeholders simultaneously”[1]. It is a much broader concept than charity, dealing with all the dimensions of a business operation in a socio-cultural environment. It is beneficial for the betterment of the performance of the business.

The term CSR is nothing new and has always been an integral part of the Indian tradition. It is similar to the idea of trusteeship advocated by Mahatma Gandhi. He regarded Indian companies and industries as the “temples of modern India” and urged them to come forward for the socio-economic growth of the nation, thereby uplifting the weaker sections of society. The government considers CSR as a business’s contribution towards the sustainable development goals of the nation.

RESEARCH METHODOLOGY

In order to analyze the term “corporate social responsibility” (CSR) and its current trends in India, the research for this descriptive paper is based on primary as well as secondary sources. In this research study, secondary sources of information such journals and websites are cited in addition to primary sources such as statutes, rules, and MCA guidelines.

CORPORATE SOCIAL RESPONSIBILITY- Understanding the concept

Corporate social responsibility is a company’s obligation towards the society. The World Business Council for Sustainable Development has defined CSR as “the continuing commitment by business to behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well as the local community and society at large[2].” According to Dr. Kurian John, “CSR is Humanitarianism,

not Charity but social and moral obligation towards each and every individual and institution[3].”

The Green Paper of European Commission (2001) has expressed it “as a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis[4].”

It can be understood from the various definitions mentioned above that CSR is not charity but something beyond that. Being socially responsible means not only fulfilling the legal obligations but also working towards the development of the community as well. In countries where there are no legal regulations, businesses shall work ethically and voluntarily towards the benefit of all. A business is responsible not only for the external environment but also for its internal environment, i.e., for the improvement of its employees, working conditions, and increasing productivity with enhanced quality as well.

THE EVOLUTION OF CORPORATE SOCIAL RESPONSIBILITY IN INDIA

The terminology “corporate social responsibility” was first introduced in 1953, when the American economist Howard Bowen published his book ‘Social Responsibilities of the Businessman’. In his writings, Bowen identifies the potential of businesses and their influence on society. He therefore argued that ‘businessmen should pursue policies that are beneficial for the common good’.[5] In India, the term CSR is recently introduced, but the concept of giving back has always been an inherent in our Indian culture and tradition. Indian scriptures have at various points mentioned the importance of sharing one’s earnings with the underprivileged segment of society.

The development of CSR in India can be divided into four phases[6]:

The first phase acknowledges the period driven by religious values, culture, and tradition along with industrialization. The merchants were involved in the construction of temples, the setting up of religious and educational institutions, providing alms to the needy, using only as much as required, and donating the rest. With the advent of Colonial Rule in 1850, the concept of CSR started changing.

The second phase is that of India’s struggle for independence. During that period, the industrialists were under pressure to support society, marking their contribution to India’s freedom struggle. Gandhi developed the idea of trusteeship and encouraged the industrialists and business houses to create trusts for educational and training institutions.

In the third stage, from 1960 to 1980, CSR was affected by the growth of the public sector.

Strict private sector regulations led to corporate misdemeanor which further led to the passage of laws on corporate governance, environmental, labor and other related issues. The failure of PSUs led to a transition from the public to private sector and its active participation in socio-economic growth. In 1965, academics, politicians, and entrepreneurs founded a National Workshop on CSR, which emphasized social responsibility and transparency.

In the fourth stage from 1980, Indian companies included CSR into their sustainable business strategies. Globalization and liberalization in the 1990s increased the dynamics of industrial growth and enabled companies to further contribute to social accountability.

“What started as a charity is now understood and accepted as a responsibility”.

IMPACT OF CSR ON A COMPANY’S PERFORMANCE

Today, several successful companies use social responsibility policies to contribute to society and show appreciation to their clients. As CSR activities are voluntary, various companies may feel obligated to get involved. Nevertheless, corporations need to prioritize such responsibility for a variety of reasons.

- CSR Boosts Brand’s Impression: Intoday’s highly competitive commercial world, it is hard for businesses to hide their activities from their clients’ eyes. Companies that firmly engage themselves in social responsibility activities develop a better stage and get prospective customers.CSR acknowledges critical issues while creating a better discourse around itself. It is a great marketing tool and also creates trust in the long run.

- CSR Leads to More Customer Engagement: Various CSR activities require businesses to engage directly with different segments of society who may be future clients. They can obtain instant opinions on the goods and services that they deal in. Additionally, brands are often spread through word-of-mouth publicity from consumers who benefit from corporate social responsibility.

- CSR is Crucial for Client’s Loyalty: CSRaidsbusinesses in developing trust to build a positive reputation and to hold clients and their loyalty. Consumers want brands to contribute to society’s welfare and become loyal when satisfied.

As per “2015 Nielsen survey”, most of the consumers are ready to pay more if a business prioritizes sustainability[7].This shows that consumers usually prefer businesses that do not focus only on profits.

- CSR Saves Cost: As already mentioned above, many customers are desirous of spending more on the products of a welfare-oriented company, leading to economies in operations. CSR policies also help in the selection of employees, thereby controlling employee turnover. Thus, the overall cost of a firm is reduced by undertaking CSR activities.

- CSR Depicts a Sense of Security for Investors: Socially responsible companies attract more investors. An investor in a company has two goals: to get a better return on investment and to appreciate the amount invested. panies that use their finances effectively while giving back to society trade responsibly and openly.

According to a “2016 Aflac report,” investors do not consider CSR spending a loss of money but rather a “sign of a firm culture less prone to costly missteps like financial fraud”[8]. “According to the survey, 61 percent of investors perceive CSR as a sign of ‘ethical company behavior that reduces investment risk’”.[9]

LEGAL FRAMEWORK GOVERNING CSR IN INDIA

It is commonly acknowledged that inclusive growth plays a significant role in India’s quest for prosperity. As a first step toward the notion of business responsibilities, the Ministry of Corporate Affairs released the “Voluntary Guidelines on Corporate Social Responsibility, 2009.[10] From this, the ‘National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Corporations, 2011’ were refined further. These guidelines, which are essentially a set of nine principles, provide Indian firms with a framework and an approach to promote responsible corporate action. The NVGs were updated and published as “National Guidelines on Responsible Business Conduct” (NGRBC) in March 2019 to demonstrate alignments with the “UN Sustainable Development Goals” (SDGs), “UN Guiding Principles on Business & Human Rights” (UNGPs), “UN Paris Agreement on Climate Change”, and other national and international developments in the field of sustainable business since 2011. The NGRBC provides the firms with a framework to address stakeholder concerns and promote fair and sustainable growth.

These guidelines[11] include the following principles that businesses should:

- “conduct and govern themselves with integrity in a Ethical, Transparent and Accountable manner.

- provide goods and services that are safe and contribute to sustainability throughout their life cycle.

- respect and promote the well-being of all employees, including value chains.

- respect the interests of and be responsive to all their stakeholders, especially those who are disadvantaged, vulnerable and marginalized.

- respect and promote human rights.

- respect and make efforts to protect and restore the environment.

- when engaging in influencing public and regulatory policy, do so in a responsible and transparent way.

- promote inclusive growth and equitable development.

- engage with and provide value to their consumers in a responsible manner.”

THE COMPANIES ACT, 2013

Section 135 of the Companies Act, 2013 deals with CSR and became effective from 01.04.2014.

- APPLICATION OF SECTION 135

“Section 135 of Companies Act, 2013 read with Rule 3 of Companies (CSR) Rules, 2014” applies to all the companies including the holding and subsidiary companies as well as foreign companies whose branches or project offices in India which fulfills the requisites stated below.

1.” Net worth of rupees five hundred crore or more, or

2. Turnover of rupees one thousand crore or more, or

3. A net profit of rupees five crore or more.”[12]

Under Rule 2(f) of the companies(corporate social responsibility) rules, 2014, “Net profit” means “the net profit of a company as per its financial statements, but shall not include the following, namely :-

(i) any profit arising from any overseas branch or branches of the company, whether operated as a separate company or otherwise; and

(ii) any dividend received from other companies in India, which are covered under and complying with the provisions of section 135 of the Act:

As per the second proviso to rule 2(f), in case of a foreign company net profit means the net profit of such company as per profit and loss account prepared in terms of clause (a) of sub-section (l) of section 381 read with section 198 of the Act”.

- CSR SPENDINGS

Section 135(5)[13] states that, “The Board of every such company, shall ensure that the company spends, in every financial year, at least two per cent. (2%) of the average net profits of the company made during the three immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy.”

The calculation of Average net profit for this section shall be done in accordance with section 198 of the act.

Furthermore, in accordance with Rule 3, a company that does not meet the requirements of Sub-section 1 of Section 135 and ceases to be covered by Section 135(1) for a consecutive period of three years is exempt from Section 135 compliance. A company is prohibited from spending money on anything that does not align with or comply to the activities that come within one of the subjects or areas listed in Schedule VII of the Act.[14].

The board of a company is in charge of ensuring that administrative overhead costs do not exceed 5% of the total amount allocated to corporate social responsibility for the relevant fiscal year. Any surplus arising from CSR activities will be kept apart from a company’s total business profit and used to support the project directly or are transferred into the Unspent CSR Account.

The company’s remaining CSR funds must be used within six months of the end of the fiscal year, either in line with the company’s CSR policy or the annual action plan, or transferred to one of the funds specified in Schedule VII. [15]

- CSR POLICY

The Board of Directors is empowered to approve CSR policies under Section 135(4) read in conjunction with Rule 6 after taking into account the recommendations of the CSR Committee and making sure that the company’s activities are in accordance with its CSR policy and pertain to the topics listed in Schedule VII of the Act.

A list of the CSR projects or programs that a business intends to implement under the categories listed in Schedule VII of the Act, along with information on the projects’ or programs’ mode of execution, implementation timelines, and monitoring procedures, should be included in the CSR policy. Additionally, it must state that any excess resulting from CSR initiatives, programs, or activities will not be included in a company’s business earnings.[16]

- ACTIVITIES ELIGIBLE FOR CSR EXPENDITURE- SCHEDULE VII

Schedule VII specifies the activities which may be included by companies in their Corporate Social Responsibility Policies. The Act’s amended Schedule VII has a comprehensive list of items that are meant to encompass a variety of activities. “The CSR projects or programs or activities undertaken in India only shall amount to CSR Expenditure”[17]. These are activities related to:

“(i) eradicating poverty, starvation, and malnourishment; advancing health care, especially preventative medicine and sanitation; supporting the Central Government’s Swatch Bharat Kosh initiative; and providing access to clean drinking water;

(ii) promoting livelihood improvement initiatives and education, including specific education and vocation skills that improve employment, particularly for women, children, the elderly, and people with disabilities;

(iii) Promoting gender equality, empowering women, establishing houses and hostels for women and orphans, establishing senior citizen facilities such daycare centers and old age homes, and taking steps to lessen the disparities that socially and economically disadvantaged groups must contend with;

(iv) guaranteeing ecological balance, biodiversity preservation, animal welfare, agroforestry, conservation of natural resources, and preservation of soil, air, and water quality, including funding the Central Government’s Clean Ganga Fund, which aims to revitalize the Ganga river;

(v) Preservation of the nation’s artistic and cultural legacy, encompassing the repair of historically significant structures and artwork, the establishment of public libraries, and the encouragement and growth of customary crafts and handicrafts;

(vi) Policies and programs that support veterans of the armed services, widows of war and their families, veterans of the Central Armed Police services (CAPE) and Central Para Military Forces (CPMF), and their families, including windows;

(vii) Training aimed at advancing Olympic, Paralympic, national, and rural sports recognition;

(viii) Contributions to the PM CARES Fund, the Scheduled Castes and Tribes Fund, or any other fund established by the Central Government for the socioeconomic development, relief, and welfare of women, minorities, and other underprivileged groups;

(ix)

(a) Contribution to research and development projects in the fields of science, technology, engineering, and medicine that are funded by the federal government, state governments, their agencies, or public sector undertakings; and

(b) Contributions to publicly funded universities, institutes of technology, national laboratories, autonomous bodies established under the Department of Atomic Energy (DAE), Department of Biotechnology (DBT), Department of Science and Technology (DST), Department of Pharmaceuticals, Ministry of AYUSH, Ministry of Electronics and Information Technology, and other bodies, such as the Defense Research and Development Organization (DRDO), Indian Council of Agricultural Research (ICAR), Indian Council of Medical Research (ICMR), and Council of Scientific and Industrial Research (CSIR)

(x) Rural development projects;

(xi) Slum area development, where “slum area” refers to any place designated as such by the central government, state governments, or any other appropriate authority in accordance with any currently enacted laws;

(xii) Disaster management, encompassing actions related to relief, recovery, and reconstruction.”

In a circular dated May 5, 2021, the Ministry of Corporate Affairs made it clear that, for the fiscal years 2020–2021–2022-203–2023, CSR funds may be used for the following purposes: ‘building health infrastructure for COVID care’; ‘establishing medical oxygen generation and storage plants’; ‘manufacturing and supply of Oxygen concentrators, ventilators, cylinders and other medical equipment for countering COVID-19’; or similar activities. Moreover, contributions to specific R&D initiatives, public funding universities, and specific organizations that carry out scientific, technology, engineering, and medical research qualify as acceptable CSR activities.[18]

However, while choosing the CSR activities to be undertaken , “preference would need to be given to local areas and the areas around where the company operates.”[19]

- ACTIVITIES NOT TO BE ALLOWED FOR CSR EXPENDITURE

Certain activities are deemed as ineligible for CSR. They are:

i. the activities carried out in the regular course of company’s business .[20]

ii. As per Clarification[21] issued by MCA on 18th June, 2014:

• One-time events that don’t qualify as CSR expenditures include marathons, awards, charitable contributions, advertisements, TV show sponsorships, etc.

• The company’s costs incurred to comply with any Act, statute, or regulation do not qualify as CSR expenditures.

iii. Any direct or indirect contribution in money to a political party is not regarded as a CSR endeavor.

iv. In compliance with section 135 of the Act, CSR initiatives, programs, or activities that solely benefit the company’s employees and their families shall not be deemed CSR activities.[22]

- CSR IMPLEMEMTATION

The Board of Directors is responsible for making sure that the CSR initiatives are carried out correctly. The following approaches can be used to adopt CSR policies:

1. Through the corporation itself, or

2. With assistance from any of the organizations listed below:

- “Section 8 Companies,” “registered societies,” or “registered public trusts” under Income Tax Act, 1961, Sections 12A and 80G, respectively, founded by the companies alone or in conjunction with another firm.

- Companies formed in accordance with Section 8 of the Act, as well as registered trusts or societies founded by the central or state governments.

- An organization created by a parliamentary act or a state legislature.

- Section 8 Companies of the Act, or registered public societies or registered trusts under Sections 12A and 80G, respectively, of the Income Tax Act, 1961, and having a minimum of three years’ experience in carrying out such operations.

With effect from April 1, 2021, the aforementioned entities that plan to engage in CSR activities must register with the Central Government by submitting the Form CSR-1 to the Registrar. [23]

- CSR COMMITTEE

If a company meets the requirements of Section 135(1) of the Companies Act, 2013, it may also form a CSR committee. However, if a company’s spending on corporate social responsibility (CSR) does not reach fifty lakh rupees, there is no need to form such a committee; in these situations, the Board of Directors will carry out the duties of the CSR Committee.

Three or more directors, at least one of whom must be an independent director, should make up the CSR Committee. If an independent director is not necessary, the CSR Committee of an unlisted public company or a private corporation may function without one.

The committee’s responsibilities are as follows:

- It will create and suggest a CSR policy to the Board of Direvtors.

- It will make recommendations regarding how much money should be expended on the CSR activities of the company.

- It will periodically monitor the CSR policy of the Company.

- It will oversee the implementation of the CSR activities the company by creating a transparent control mechanism.

- DISCLOSURE REQUIREMENTS

It is mandatory for companies to disclose a report on CSR in their board report annually. It includes CSR policy, CSR Expenditure, Composition of CSR committee, etc. The Board Report must include an explanation if the company has not been able to devote the minimum amount of funds to its CSR projects. The companies having a website, must make their CSR policy and the report containing details of such activities accessible on their websites for various purposes.

Businesses that have websites are required to provide access to their CSR policy and the report that includes specifics about these actions.

The Companies (CSR Policy) Amendment Rules, 2021 were notified by the Ministry via notification dated 22.01.21, introducing the Impact Assessment tool, in order to assess and evaluate the success and results of the CSR initiatives. An independent agency must conduct impact assessments on behalf of the designated companies. In order to uphold transparency and accountability, these reports must be presented to the Board and appended to the yearly report on corporate social responsibility. In addition, it required businesses with unspent CSR funds to form a CSR committee regardless of the size of the obligation amount.

RECENT TRENDS OF CSR IN INDIA

CSR has become a great business strategy around the world. With the mandatory provisions of the Companies Act, 2013, “there is an increase in the CSR expenditure of Indian Companies with almost INR 8800 Crores of CSR spend in the 1st reporting year of CSR compliance.”[24]

From CSR data analysis, it can be understood that education, healthcare, and rural development are the top three sectors receiving CSR funds since the implementation of the CSR legislation. “The data of the last seven years, i.e., 2014-15 till 2020-21 shows that, based on company filings in the MCA21 registry, the education sector received nearly Rs. 47187.68 crores (including education, livelihood enhancement projects, special education, and vocational skills), which amounts to approximately 37% of the total CSR expenditure”[25]. “The health sector (including health care, poverty, eradicating hunger, malnutrition, sanitation, and Swachh Bharat Kosh) is the second sector, with 30% of the CSR expenditure amounting to Rs. 38011.49 crores”[26]. Also, “more than Rs. 12,300 crores were spent on Rural development projects, which accounted for 9.6% of the total CSR expenditure.”[27]

The data reveals that in FY 2020-21, “the CSR funds (over 44%) went to 10 states in India. These states include Maharashtra, Gujarat, Andhra Pradesh, Karnataka, Uttar Pradesh, Tamil Nadu, Rajasthan, and Madhya Pradesh.”[28]

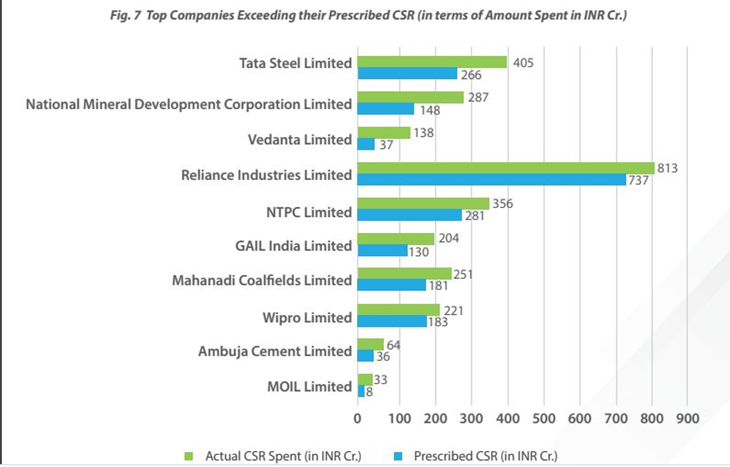

As per the “Indian CSR Outlook Report of 2022,” Tata Steel Ltd. is at the top of the list of large companies exceeding their CSR spending in the Financial Year 2021-22.[29]

The total spending on CSR in FY 2021 was Rs. 26,210 crore, nearly twice as much as in FY 2016, when Rs. 14,542 crore was spent. This suggests that CSR expenditure is rising in India. But the effect of the CSR funding is not generally felt, and it’s important to increase the impact and visibility of these invested funds.[30]

CHALLENGES FACED IN CSR IMPLEMENTATION

CSR in India has grown significantly; however, there are certain challenges that need to be addressed, such as the lack of transparency and accountability, the lack of society’s involvement, the lack of common agreement on the implementation of such activities, the lack of alignment of CSR activities with the development priorities of the country, the lack of requisite economic resources, local proficiencies, and infrastructure, greenwashing at the national scale, and the lack of participation from SMEs. With the right approach and implementation, CSR can play an even better role in the overall development of India.[31]

RECOMMENDATIONS[32]

CSR in India has the strength to bring about positive outcomes for communities, To enhance the positive impact of CSR in India, the following recommendations can be considered:

- Increased accountability and transparency: Businesses should be more open about their CSR initiatives, including how they use funding, interact with the community, and what kind of impact they are making.

- Better coordination and oversight: CSR activities need to be more effectively planned and overseen. This can be achieved by building a national CSR database that monitors business activity and evaluates its effects.

- Resolving underlying structural difficulties: CSR programs must concentrate on resolving structural issues that are at the root of social and environmental challenges.

- Sustainability Reporting: Sustainability reporting is becoming increasingly important due to the greater awareness of sustainability-related matters. The Global Reporting Initiative has offered a framework for sustainable reporting.

- Government’s role: The government should collaborate with companies to create a clear set of standards for CSR and to make companies answerable for their CSR initiatives. This will help ensure that CSR efforts are having a positive effect and that companies aren’t using CSR to avoid taxes. It may also give awards to the companies that are helping society.

- CSR as part of business: Companies should include CSR in their business strategies rather than treating it as a stand-alone activity. This will ensure that CSR aligns with the company’s overall objectives and is having a positive effect on society.

CONCLUSION

“Corporate Social Responsibility” (CSR) is an idea of greater good for society. All the companies, being legal persons, have a responsibility towards the development of the society from which they prosper. The future of CSR is very promising. CSR activities are never-ending, continuous processes that have a positive impact on a company. It is necessary to achieve long-term sustainability in the global economy. CSR is mandatory for all companies, and its growth is regulated so that the ultimate goal can be achieved through the Companies Act, 2013. CSR helps a company grow and make a good name in the world, along with the growth of the country.

AUTHORED BY: SAMRADDHI MUTHA

RENAISSANCE LAW COLLEGE, INDORE

[1]United Nations Industrial Development Organization, https://www.unido.org/our-focus/advancing-economic-competitiveness/competitive-trade-capacities-and-corporate-responsibility/corporate-social-responsibility-market-integration/what-csr

[2] World Business Council for Sustainable Development (2000), https://www.gaea.bg/about-GAEA/corporate-social-responsibility.html

[3] KURIAN JOHN MELAMPARAMBIL’S THEORY OF SOCIAL RESPONSIBILITY, https://www.melamcharities.org/csr

[4] European Commission, Green Paper-Promoting a European Framework for Corporate Social Responsibility, 6 (2001), https://op.europa.eu/en/publication-detail/-/publication/18607901-76e9-47ea-91f8-436a4f412450/language-en

[5] Casey Schoff, The Evolution of Corporate Social Responsibility, https://www.ecolytics.io/blog/evolution-of-csr.

[6] How has CSR evolved in India?, https://www.soulace.in/how-has-csr-evolved-in-india.php

[7] Nielsen Media Research (2015) https://www.nielsen.com/us/en/insights/reports/2015/the-sustainability-imperative.html. Accessed Jun. 26 2018

[8] Sneha Sengupta, Corporate Social Responsibility in India: A Constitutional and Theoretical Commentary (October 17, 2021), WWW.Lawoctopus.com.

[9] https://www.aflac.com/docs/about-aflac/csr-survey-assets/2016-csr-survey-deck.pdf, visited on Jun. 1,

2020.

[10] History, https://www.csr.gov.in/content/csr/global/master/home/aboutcsr/history.html

[11] National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business, 2011,Ministry of Corporate Affairs, https://www.mca.gov.in/Ministry/latestnews/National_Voluntary_Guidelines_2011_12jul2011.pdf

[12] Companies Act,2013, Section 135, No. 18, Acts of Parliament, 1956 (India).

[13] Companies Act,2013, Section 135, No. 18, Acts of Parliament, 1956 (India).

[14] Rule 7, Companies (Corporate Social Responsibility) Rules,2014.

[15] Ministry of Corporate Affairs, CSR Amendment Rules,2021, https://cleartax.in/s/csr-amendment-rules-2021.

[16] Rule 6, Companies(Corporate Social Responsibility) Rules, 2014.

[17] Rule 4, Companies(Corporate Social Responsibility) Rules, 2014.

[18] Ministry of Corporate Affairs, General Circular No. 09/2021, www.mca.gov.in, https://www.mca.gov.in/Ministry/pdf/GeneralCircularNo9_05052021.pdf

[19] Companies Act,2013, Section 135, No. 18, Acts of Parliament, 1956 (India).

[20] Proviso to Rule 6(1), Companies (Corporate Social Responsibility) Rules,2014.

[21] Ministry of Corporate Affairs, General Circular No. 21/2014, www.mca.gov.in, https://www.mca.gov.in/Ministry/pdf/General_Circular_21_2014.pdf

[22] Ministry of Corporate Affairs, FAQ on CSR cell, www.mca.gov.in, https://www.mca.gov.in/mca/html/mcav2_en/home/home/efacilitaion+center/faq+on+csr+cell-site+area/faq+on+csr+cell.html

[23] Ministry of Corporate Affairs, CSR Amendment Rules, 2021, https://cleartax.in/s/csr-amendment-rules-2021

[24] The Big Picture of CSR in India, CSRBox, https://csrbox.org/CSR-in-India.

[25] Unveiling CSR Trends: A step towards Sustainability, Ministry of Corporate Affairs, Monthly Newsletter, Volume 66, May 2023.

[26] Ibid.

[27] Ibid.

[28]Ibid.

[29] 8th Annual India CSR Outlook Report, 2022, CSRBOX and NGOBOX, https://csrbox.org/media/CSRBOX-India-CSR-Outlook-Report-2022_Full-version.pdf.

[30] Unveiling CSR Trends: A step towards Sustainability, Ministry of Corporate Affairs, Monthly Newsletter, Volume 66, May 2023.

[31] Rabinarayan Samantara and Shivangi Dhawan, Corporate Social Responsibility in India: Issues and challenges, IIMS Journal of Management Science 11(2):91-103, May 2020.

[32] Ibid.