Abstract

The main objectives of this article are to examine how cryptocurrencies function in the money laundering process and the potential and constraints of doing the same.

Cryptocurrencies are used in many international transactions and purchases, but they don’t have a standard definition or official legal status. In addition, the state of affairs complicates the criminal investigation of money laundering involving cryptocurrencies. Because of this, it is difficult for law enforcement to locate criminals and present proof of their crimes. Furthermore, covered in this article are two fundamental concepts associated with cryptocurrencies: anonymity and decentralization.

This study looks at the historical development of cryptocurrencies, starting with Friedrich August von Hayek’s idea of “currency independent from banks and governments” and ending with the creation of decentralized currencies. Several cryptocurrency frameworks from around the world have been compared concerning India as part of the study. This study suggests that cryptocurrency is an ideal tool for money laundering because it gives its owner some anonymity because it doesn’t need location or personal information. By using this feature, there is a reduced chance that criminal activity will be recognized and pursued by law enforcement. Additionally, because banks, governments, and non-governmental organizations are not obligated to verify cryptocurrency transactions, governments are powerless to control them. A user can manage several accounts at once and conduct transactions from various locations.

In a notification published on March 7, the government stated that transactions involving cryptocurrency assets were subject to the Prevention of Money Laundering Act.

Despite current anti-money laundering laws now covering the aspect of cryptocurrency still it’s not sufficient enough to address aspects of blockchain technology like stake, security, or identity verification, this thesis offers solutions to control the problem of money laundering through cryptocurrency use.

This thesis discusses how India has failed to meet international standards for anti-money laundering regulation and shows that current international norms do not fully regulate cryptocurrencies about the risk of money laundering.

Keywords

Money Laundering, Blockchain technology, Cryptocurrency, Bitcoin, White-collar crimes.

Research Methodology

The thesis first examines crypto asset restrictions’ efficiency in India and other countries using the functional technique. The legal comparison focuses on commercial restrictions and possible criminal wrongdoings by groups or individual criminals, including money laundering. Such a comparison sheds light on the viability and applicability of current legislation in India.

Secondly, this thesis examines the consistency of present crypto asset legislation in addition to commercial operations using the analytical method. Fintech’s rapid growth has added to the complexity of many countries’ regulatory frameworks. Authorities, on the one hand, are the primary bodies in charge of ensuring financial stability, market integrity, and consumer protection. As a result, severe rules may be warranted.

In summary, the thesis uses theoretical approaches and comparative analysis to assess the efficacy and coherence of Indian laws and regulations regarding commercial and non-commercial crimes involving crypto assets. Furthermore, “the common-core method” approach (one of the comparative methods) contains both the functional and analytical methods, allowing for a thorough analysis of the efficacy and consistency of present rules in India, the United Kingdom, the United States, and Australia.

Review of Relevant Literature

Jackobi (2018) The study evaluated the global AML system from a security governance viewpoint and concluded that anti-money laundering represents the aspects of security governance.

Pol (2018). The study added to this body of knowledge by concentrating on AML practices and their effectiveness as a policy against FATF-defined outcomes. FATF approaches are ineffective, according to him, and greater implementation is required to generate beneficial results. Further, questioned whether forfeiture of illicit assets is a good measure of measuring the efficacy of AML rules and if their extension as a requirement for new industries will have an effect, as well as the other assumptions on which the global AML/CFT framework is founded.

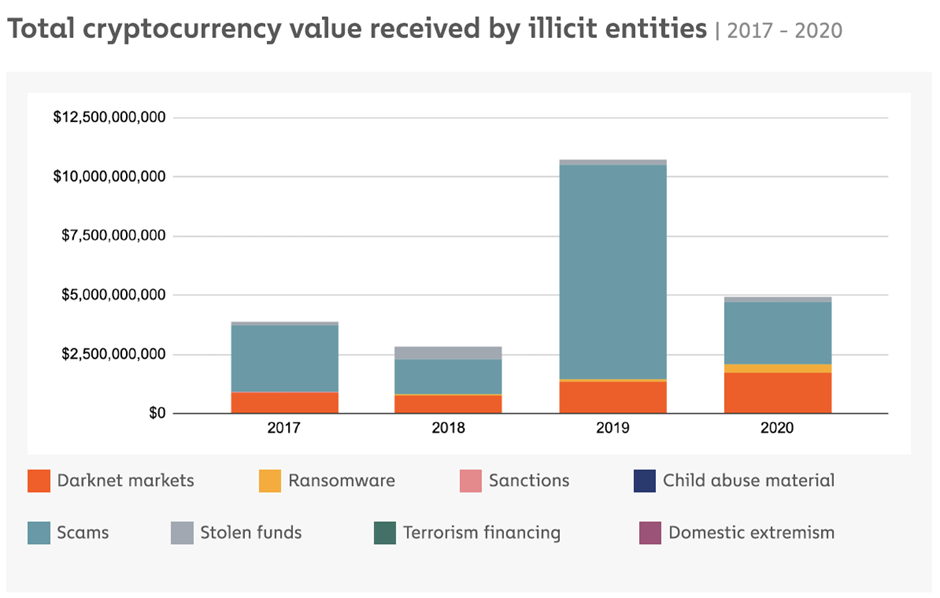

Chitesh Rai Tuli (2017). The current article is about Ransomware which according to the author has origin way back in 1989. Currently, there was a Petya attack in June 2017, and thus over the years Ransomware has not stopped but has evolved itself. The first attack for Ransomware was conducted on Cyborg Corporation where demand was made to unlock files. Those days the encryption on files was not very strong, Ransomware funds were traceable, and application of the computers to store all and sundry data was not there. In today’s time, the files encrypted are complicated to unlock. The transfer of funds by way of Cryptocurrencies has made things very easy for hackers to collect funds untraced from law and computers store large data and programs on which the companies run.

From the above literature, a huge wealth of Knowledge is gained and gives an insight into the quantum and nature of work done so far about Bitcoins and money laundering.

Money Laundering Using Cryptocurrencies.

Cryptocurrency money laundering is using virtual currencies to hide the source and ownership of illegal funds. Here are a few typical techniques:

1. Mixing Services: To compile cryptocurrency transactions from various sources, criminals utilize mixing, also known as tumbling, services. It becomes difficult to identify the source when these services combine the funds and send them to different addresses.

2. Cryptocurrency Exchanges: To convert illegal funds into cryptocurrencies, criminals may use unregulated or anonymous cryptocurrency exchanges. They can conceal the funds’ source and add another layer of anonymity by doing this.

3. Layering: Through a network of middlemen, fraudsters move money between various cryptocurrency wallets and exchanges by conducting a large number of transactions.

As a result, investigators find it difficult to adhere to the compliances.

4. Integration with Lawful Sources: Illegal investors or enterprises may be integrated using money obtained through criminal activity. They might buy assets like real estate or luxury goods with cryptocurrency, or they might use it to start legitimate businesses, all of which would appear to be legal transactions.

5. Initial Coin Offerings (ICOs): By issuing tokens, scammers can raise money through ICOs.

Initial coin offerings, or ICOs, are portrayed as lucrative business opportunities for investors.

Nevertheless, the money raised is frequently embezzled or used as a pretext to spend money that isn’t legal.

Anti-money laundering (AML) regulations concerning cryptocurrencies

It aims to stop people from using virtual currencies for illegal purposes and make sure that laws against financial crime are later on. The following are some notable AML regulations that commonly deal with cryptocurrencies:

- Customer due diligence (CDD): CDD procedures are normally mandated for exchanges and cryptocurrency service providers. To do this, it is necessary to confirm the clients’ identities, gather pertinent identity documentation, and evaluate their level of risk.

- Know Your Customer (KYC): Companies that deal in cryptocurrencies are typically obliged to put KYC policies in place. Names, addresses, and other pertinent information about their clients are obtained as part of these procedures. This makes it easier to locate and identify people who transact with cryptocurrencies.

- Financial institutions, including cryptocurrency exchanges, are required to report suspicious activity (SAR).

- Transaction Monitoring: Generally speaking, it’s necessary to install reliable systems for transaction monitoring by cryptocurrency companies to follow AML regulations. These systems look for trends, abnormalities, and other signs in transaction data that might point to fraud or money laundering.

- Documentation: Companies that deal in cryptocurrencies are frequently required to maintain detailed records of every transaction with a customer, including the origin and destination of the funds. These documents can be used by the authorities to back up their investigations and audits.

- International Cooperation: AML regulations usually place a high value on information exchange and cross-jurisdictional cooperation. Governments and regulatory bodies collaborate to prevent cross-border money laundering associated with cryptocurrencies.

Legal concerns and position of cryptocurrency in India

Constitution of India

According to Article 246 read with the 7th Schedule, the federal government and the states have equal authority to regulate and control Bitcoins and other cryptocurrencies. Although they aren’t specifically mentioned, bitcoins fall under the heading of “other similar instruments.”

Three laws/acts—the RBI Act, the Coniage Act, and the FEMA—define the legal status of cryptocurrencies. For this reason, learning more about this status is crucial to fully comprehending cryptocurrencies. Together, these three statutes contribute to the definition and control of money, as well as the creation, use, and consumption of money. It is significant to note that the terms “legal tender” and “banknotes” are not mentioned in any of these three statutes.

Currency

The RBI lacks a definition of currency. However, foreign currency is defined in the FEMA Act. Any banknotes, drafts, money orders, traveler’s checks, postal orders, and others as decided by RBI by FEMA, checks, and other similar instruments. Foreign currency is something that is not considered Indian money. One-rupee coins and special banknotes issued in compliance with RBI Act Section 28 are not included in this definition.

Legal tender

The term “legal tender” is still not defined in Indian law. The Reserve Bank of India was given the sole authority to print banknotes. As a result, the RBI’s banknotes are covered by Section 26 of the RBI Act of 1934 and are accepted as legal tender in India.

Currency Notes

Currency notes are defined as money in the form of coins and banknotes in Section 2(i) of the F.E.M.A. According to this interpretation, cryptocurrencies such as bitcoins do not satisfy this requirement because they are not issued in compliance with the RBI Act or the Coinage Act. Section 22 of the RBI Act of 1934 states that the Reserve Bank of India has the sole authority to issue bank notes, and Section 26 states that coins and notes issued by the RBI are recognized as legal tender in India. The bill will not grant Bitcoins or other cryptocurrencies the status of banknotes or other legal tender because they are not issued by the RBI. Money and banknotes do not meet the requirements for legal tender because they are not legal tender.

Virtual Currency– Are virtual currencies considered to be money in India? Do other cryptocurrencies, such as Bitcoins, qualify as currencies? Indian courts uphold the maxim “express um facit cessare taciturn,” which asserts that anything not expressly stated is excluded. was mentioned in the case of Shankara Rao Badam v. State of Mysore (1969) and Union of India v. Tulsiram Patel (1985). In light of the foregoing, Bitcoins and other cryptocurrencies are not defined as currencies and thus cannot be referred to as such. It can, however, be placed under the definition of such other similar instruments under section 2(h) of the RBI Act it appears that RBI will need to issue a notification to place Bitcoins and other Cryptocurrencies under the purview of Section 2(h) of the Act.

Regulatory Concerns Regarding Cryptocurrencies in India

In a notification published on March 7, the government stated that transactions involving cryptocurrency assets were subject to the Prevention of Money Laundering Act. Despite current anti-money laundering laws now covering the aspect of cryptocurrency still it’s not sufficient enough to address aspects of blockchain technology like stake, security, or identity verification, this thesis offers solutions to control the problem of money laundering through cryptocurrency use. The R.B.I. until April 2018, had adopted a hands-off stance due to the Central Government’s policy being delayed. On the other hand, the RBI prohibited banks from providing banking services to people or organizations that traded cryptocurrencies in India with a notification published on April 6, 2018. It had always warned that although money laundering could lead to legal action, the government would not be notified of such an advisory. It appears to be in the observe and hold condition.

Due to possible legal and security issues, it has so far issued advisories cautioning against handling and storing Bitcoins and other cryptocurrencies.

According to reports, the RBI was keeping an eye on reports from various nations about the risks associated with cryptocurrencies, such as the potential for money laundering and poor investment opportunities. The RBI issued a warning in 2014, noting not only that mining, trading, or accepting cryptocurrency as payment was not recognized as lawful, but also the following risks.

- Digital currencies kept in e-wallets are called cryptocurrencies. There is a potential for value loss due to hacking, password loss, etc.

- Since the RBI and the Indian government have outlawed the trading, buying, or selling of cryptocurrencies, no authorized entities or exchanges will be held liable for any losses.

- If a user experiences a loss during peer-to-peer payment, they might not be able to pursue legal action.

- The so-called exchanges in India engage in illegal activity because there are no authorized exchanges there. Consequently, traders are also involved in illegal activity on these exchanges.

KYC

The Reserve Bank of India has instructed all banks to adhere to the KYC—Know your customer—Norms to safeguard customer accounts and ensure compliance with the Anti-Money Laundering and Countering Financing of Terrorism Act. This also holds for investments made in stocks, commodities, and other financial markets. Clients may occasionally be asked to submit KYC documentation, and if necessary, physical verification of the individual and the location may also be conducted. It is imperative that any customer who deviates from their regular payment schedule or accounts for any unusual transactions be notified right away.

Since Bitcoins are peer-to-peer in nature and are based on Blockchains with long transaction histories, they are pseudo-anonymous and cannot be used in the Indian system due to KYC reporting requirements. In India, exchanges only permit account opening after KYC requirements have been satisfied. It is mandatory for banks and other financial institutions to gather transactional data about their clients and to provide it to law enforcement when there is a reason for concern.

Section 3 of the Prevention of Money Laundering Act, 2002 (the “PMLA”) defines the act of money laundering. In PMLA Section 3, the word “cryptocurrency” was recently added. Peer-to-peer exchanges keep the trade secret from outside parties, which may impede the flow of information to the agencies about tainted or suspicious transactions.

Therefore, it would appear that new legislation as well as amendments to related acts will be needed to address the issues raised by these and other cryptocurrencies. It also appears that the current laws are unable to effectively regulate transactions involving Bitcoin or other cryptocurrencies. On exchanges registered for cryptocurrencies in India, transactions are limited to electronic transfers only, and they are subject to strict Know Your Customer regulations. They are following the guidelines to ensure that neither they nor their clients are impacted by the laws about money laundering. It is irrelevant to ask if K.Y.C. standards as they are applied in India are sufficient to stop money laundering.

Position of virtual currencies in Foreign Countries

Different foreign nations have different views about cryptocurrencies. While some nations have welcomed cryptocurrencies and legalized them, others have issued advisories or imposed limitations on them. For example, under the Bank Secrecy Act (BSA), cryptocurrency money transmitters in the US are regulated by the Financial Crimes Enforcement Network (FinCEN). Certain cryptocurrencies are now governed by securities laws and regulations after being categorized as securities by the Securities and Exchange Commission (SEC).

The EU’s cryptocurrency regulations are outlined in the Fifth Anti-Money Laundering Directive (5AMLD). It requires custodian wallet providers and cryptocurrency exchanges to follow anti-money laundering (AML) and know-your-customer (KYC) guidelines.

According to the Payment Services Act, cryptocurrencies are accepted as valid forms of payment in Japan. The country has enforced license requirements for cryptocurrency exchanges to further protect consumers and prevent money laundering.

Suggestions and Recommendations

Global recommendations that India can put into practice

Presenting the Japan Model, where licenses are easily obtained and can be easily tracked down.

The Payment Services Act in Japan, which has the most advanced Bitcoin laws globally, recognizes Bitcoin and other virtual currencies as legitimate property (PSA).

As a result of these laws, cryptocurrency exchanges operating in Japan must apply for and comply with standard AML/CFT regulations. In December 2017, the National Tax Agency declared that gains made from cryptocurrency should be considered as “miscellaneous income” and that traders should receive the appropriate charges. The world’s largest Bitcoin market is located in Japan.

The Financial Instruments and Exchange Act (FlEA) and the PSA are two of the most recent regulations, and they will take effect in May 2020. The modifications rename “virtual currency” as “crypto-assets,” tighten regulations on crypto financial derivatives, and reinforce restrictions on managing users’ virtual money. As per the updated guidelines, the FIEA covers cryptocurrency-swapping businesses, while the PSA covers custodial internet providers for cryptocurrencies in Japan that do not purchase or sell crypto assets.

Japan Cryptocurrency Exchange Regulations

Japan has progressive laws governing bitcoin trading as well. Only companies with highly qualified financial agencies are allowed to function as bitcoin exchanges under the PSA. However, foreign cryptocurrency exchanges are required to sign if they can show proof of a corresponding enrollment guideline in their host country, to Japan’s liberal mindset.

Although exchanges are allowed in Japan, the country has become more aware of crypto regulations following several high-profile thefts, such as the infamous Coin cheque robbery of $530 million in virtual currency. The Financial Services Agency (FSA) of Japan has put a lot of effort into policing cryptocurrency exchanges within the country. The FSA must now be contacted for cryptocurrency trading to be operational, as a result of PSA amendments. Stricter guidelines for AML/CFT and information security are imposed, and this process may take up to six months. Exchange-based laws in Japan are primarily concerned with maintaining market integrity; subscribers, dealers, and exchanges must adhere to particular record-keeping requirements and submit a financial statement to the Financial Services Agency (FSA).

Adhering to FATF guidelines regarding cryptocurrency

The advantages of information assets are numerous. They could speed up, simplify, and reduce the cost of the transaction while offering options to those who cannot access traditional financial products. However, they run the risk of becoming a legitimate haven for money laundering and terrorist activities in the absence of regulatory oversight. The Financial Action Task Force (FATF) has been keeping a close eye on changes in the bitcoin industry. Several regional governments have begun to regulate the virtual currency market, and some have outright prohibited digital commodities.

However, the majority of governments haven’t taken any action yet. Terrorists and other criminals have a lot of opportunities thanks to these holes in the international regulatory framework.

With the support of the G20, the FATF has established globally enforceable standards to forbid the misuse of virtual assets for money laundering and financing terrorism. A virtual commodity is any valuable software program that can be transferred, exchanged, and used in exchange for money. There is no mention of the fiat currency digital model.

By applying the same restrictions that apply to the finance industry, the FATF guidelines guarantee that virtual resources are fairly represented. The FATF standards apply when virtual resources are converted from one digital commodity to another and when they are exchanged for fiat money.

Conclusion

To stop financial fraud, it’s critical to improve your ability to monitor commodity derivatives providers and examine digital commodities. Fighting criminal financing requires an interdisciplinary agency that works with public and private partnerships.

New technologies can help prevent financial fraud involving cryptocurrencies by being integrated into networks of illicit financing. More ways to prevent money laundering with cryptocurrencies include passing privacy laws, using “White Caps,” and allowing banks to examine currency transactions online. Cryptocurrencies are a long-term threat to the nation because they are illegal. They should be subject to the same laws that govern other currencies, and the appropriate steps should be taken.

MEGHAVI JINDAL

AMITY UNIVERSITY, KOLKATA